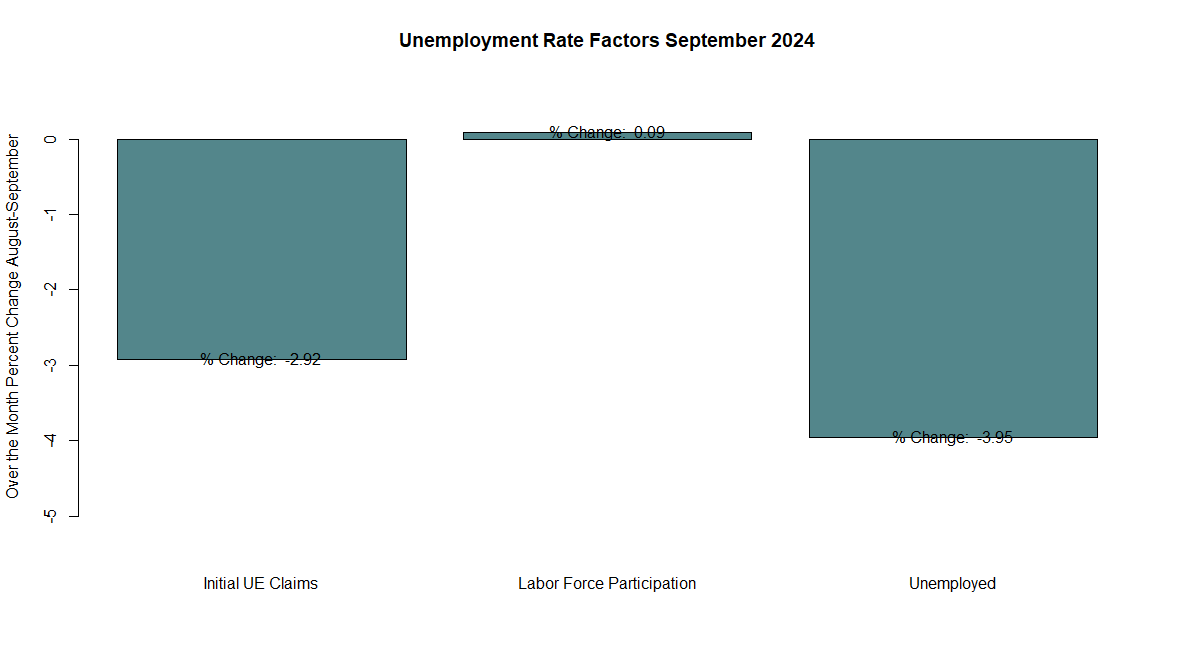

The US Unemployment Rate remained almost unchanged at 4.1% during September 2024 according to data released by the US Bureau of Labor Statistics. The factors driving the monthly change were largely the survey of households (-3.95%), which asks households about their unemployment situation, and the decrease in the monthly aggregate of Unemployment Insurance Claims (-2.9%). Labor Force Participation also helped the rate remain steady at the 4% threshold.

We do not get too excited about non-farm payroll and household survey data on the latest Unemployment Rate report. At Econometricus, we still see the same picture of the recent months, which is that the main metrics of the employment situation do not allow us to pinpoint upward risk in unemployment; instead, analysts see a strong market that seems to be in stand-by mode while the Federal Reserve decides about interest rates. In fact, the assessment of the labor market appeared and felt incomplete a few weeks ago without data to explain the spike in Unemployment Insurance in July. Thus, the only two metrics that might have set the alarms off for monetary policymakers to cut interest rates were the number of hours worked in July and the number of Unemployment Insurance Claims for the same month. The former went down significantly while the latter went up simultaneously.

September’s unemployment rate of 4.1% requires the same reasoning to assess both the state of the labor market and the effect of Jerome Powell’s further guidance at the Jackson Hole Conference, followed by the 0.50 basis points cut on September 17th. In other words, analysts need data on the number of hours worked in August and September before drawing conclusions about what looked like a cooling labor market amid summer 2024. At a recent post, we stated that,

“after the cut in hours, the firms may follow with a cut in positions. By offering forward guidance at the Jackson Hole Conference and cutting the rate by 0.50 points, Chairman Powell sought to ameliorate the apparent upward risk of unemployment by providing a strong shift in necessary expectations”

The current Employment Situation report is almost meaningless as its metrics have not currently shown relevance to shift the focus of monetary policy to the upward risk of unemployment while deferring effort on inflation (mainly the Shelter Price Index). Likewise, despite the “strong” data coming from BLS, the Federal Reserve went on to cut interest rates to incentivize investment and spending. We infer that the only reason for the Fed to make such a cut was the mentioned labor metrics. Therefore, we need to see the same statistics in the incoming releases to gauge the labor market beyond payroll “blowing expectations” headlines.

Finally, we still think the balance of risk for the dual mandate remains on Inflation. As we stated it before:

“At Econometricus, we think that the September 17th cut was unnecessary and poses a higher risk to prices. The spillover from the cut will most likely lead to a stubbornly high level of shelter prices by breaking the bottleneck in the housing market. The rate cut will inject dynamics into housing, indeed, but such dynamics will most likely lead to higher prices. We hope that more competition in housing hunting may not help drive down the Shelter Index.”

Make an Appointment se see how we can support your data flow

Categories: Macroeconomics