July’s unexpected surge in the unemployment rate drove much of the attention to the labor market as a focus in the balance of risk for monetary policy. Most of the preliminary conclusions about a weakening employment situation led both labor analysts to predict, and the Federal Open Market Committee to cut federal funds rates on September 17th by 0.50 percentage points. To get a better understanding of the facts that led to the cut outcome, analysts needed to track the number of new unemployment insurance claims, the number of separations, and the mean value of hours worked during the month. Although separations and UI claims did not set the alarms off, the Bureau of Labor Statistics’ data on average hours worked revealed that there was indeed a deep slowdown in the number of hours worked. At Econometricus, we think that although the data may demonstrate signs of a weakening labor market, a cut of 0.50 percent points is unnecessary.

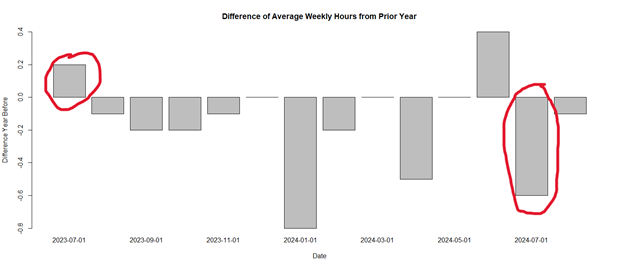

Data on Real Earnings came in with a delay of two months, though just in time for the September 17th FOMC meeting. This indicator is probably the only one showing how cooled the labor market is, apart from Separations and UI Claims. The alarming fact in Real Earnings is that for a seasonal summer month like July, the number of hours worked curbed down by more than half a percent point. Chart 1 highlights the year-over-year changes between 2023 and 2024. It is visible how in 2023 workers spent more time working, as is expected from a summer season, whereas in the same month of 2024, the decrease is almost as deep as January, one of the slowest months of the year. However, the decrease seems large given that the 2023 yearly change is inflated by the Covid-19 recession numbers from 2022 and 2021.

These data shed light on a labor market that slowed down by cutting hours of workers, without a doubt. Further, we understand the intuition that after the cut in hours, the firms may follow with a cut in positions. By offering forward guidance at the Jackson Hole Conference and cutting the rate by 0.50 points, Chairman Powell sought to ameliorate the apparent upward risk of unemployment by providing a strong shift in necessary expectations. Powell’s statement could have been enough for expectations to shift; however, there was no other way to send a message without following through.

At Econometricus, we think that the September 17th cut was unnecessary and poses a higher risk to prices. The spillover from the cut will most likely lead to a stubbornly high level of shelter prices by breaking the bottleneck in the housing market. The rate cut will inject dynamics into housing, indeed, but such dynamics will most likely lead to higher prices. We believe that more competition in housing hunting may not help drive down the Shelter Index.

The developments of data releases can be seen through this series of posts:

- Shelter Price Index jumped up to 4.95 percent

- Labor Market in need of higher expectations

- [Econometricus Nowcast] Unemployment Insurance Claims lower than ten Weeks Average

- July 2024 Job Separations Do Not Support Labor Economists’ Panic

- Still no preliminary signs of labor market weakening

- Fed’s staff see the Labor Market as rebalancing instead of weakening

Make an Appointment with Econometricus

Categories: Macroeconomics