Despite recent labor market cooldown news, data show price increases may have a greater risk than unemployment rate increases. Analysts looking to understand the balance of risk within the Federal Reserve dual mandate will have to ponder data on the effect of wage inflation over prices (mostly shelter), on the one hand; and on the other, the effect of restrictive monetary policy on unemployment. At the time of this writing, wage inflation data has shown correlation with prices while unemployment remains robust with respect to interest rates increases. The choice for rate cuts in the FOMC September’s meeting depends heavily on Wage Inflation rather than on an unlikely unemployment rate hike.

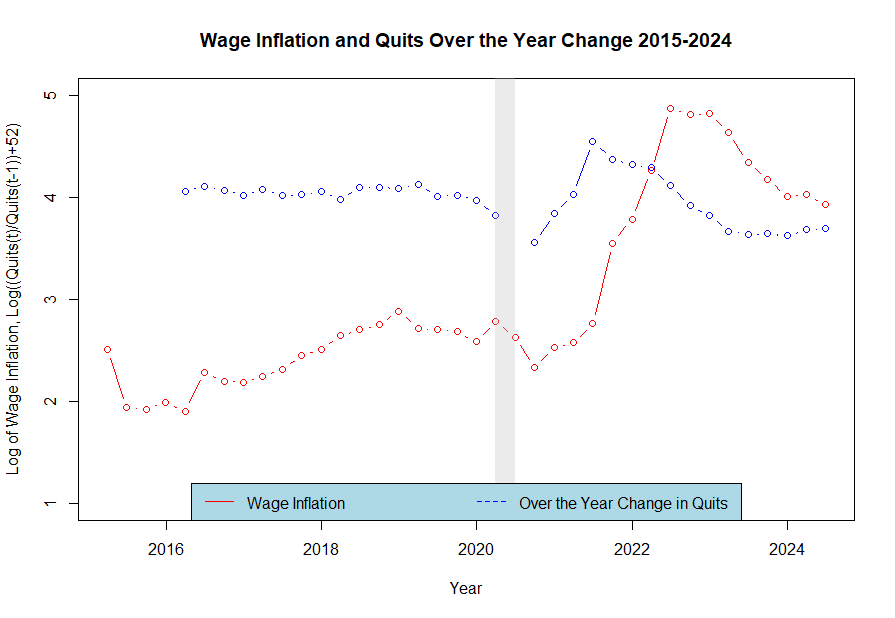

Thus far in the Covid19 Recession recovery, we know that the Pandemic triggered job quits to climb to record highs, thereby spilling over into wages (see chart below). Macroeconomists believe that an increase in wages leads to a direct increase in prices, particularly in the cost of shelter and housing. Thus, it would make sense to put the brakes on wage increases to avoid putting at risk the progress made on overall inflation. Although the Fed’s dual mandate forces us to think twice about such a conclusion, data on employment and GDP growth have proved to be resilient to the current restrictive monetary policy, which leaves price inflation risk as the priority on the Fed’s dual mandate.

The rationale behind Quits and Wages assumes that if Quits Rates return to their pre-pandemic levels, so will Wage Inflation. We put the data together to run a simple student’s t-test for differences (all statistically significant) in the mean values of both metrics and found that although Quits may get back to normal, there is no evidence to support the expectation that Wage Inflation is returning to its pre-pandemic levels any time soon. It may take more than two BLS’s Employment Cost Index/CPI/Unemployment reports to find evidence that Wage Inflation is on track to drop from the current 4.4% (2024 average) to 2.4% (pre-pandemic average).

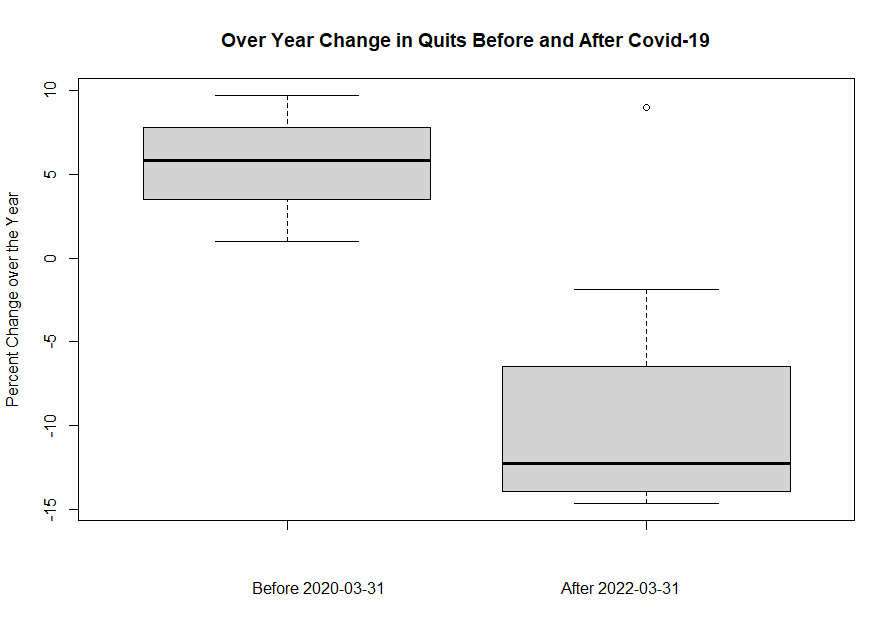

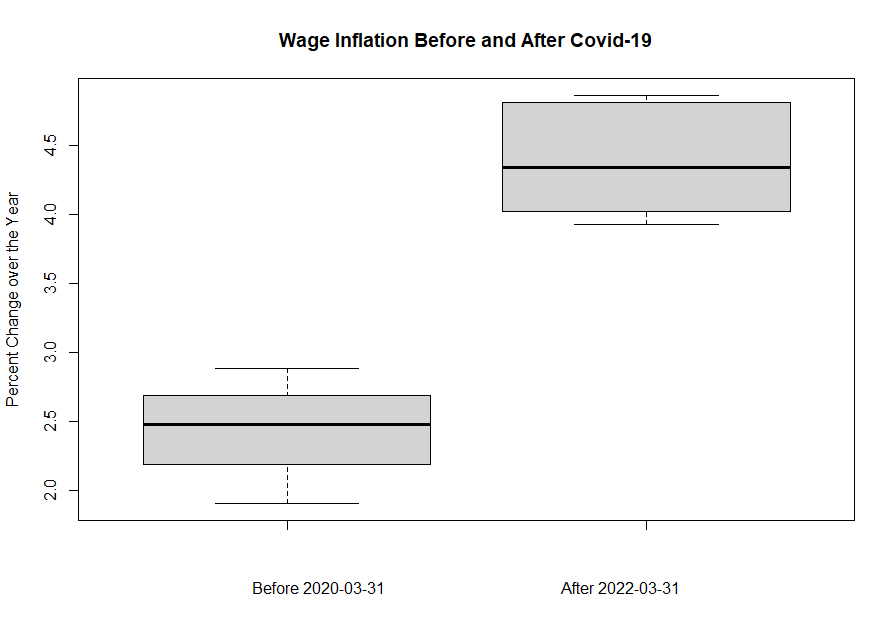

The boxplots above show the differences in the data, which make it clear that Quits have been on a steady decreasing trend, averaging -8.7 percent on a yearly basis, whereas Wage Inflation has shown its stickiness, hovering well above four percent since the third quarter of 2022. In other words, even though Job Quits have dropped, Wage Inflation remains significantly high with respect to pre-pandemic levels. Hence, if under the current restrictive policy unemployment remains unchanged at 4.1%, the only concern is inflation going above 2.9% because of wage inflation. The Fed will not let the latter happen.

Make an Appointment

Categories: Macroeconomics, Policy

1 reply »