Job separations were not any greater than any other July since 2010 – except for the pandemic years. Bureau of Labor Statistics JOLTS data release (September 4th, 2024) shed light on July’s unemployment rate uptick by revealing no signs of alarms in the US labor market. The month’s separations behaved just like any other July, thereby confirming the facts about an increase in the labor force as a major driver of the higher unemployment rate.

The current narrative about Chair Jerome Powell’s “time to adjust has come” statement was built upon a preliminary sign of a weakening labor market when July’s unemployment rate was calculated. Since then, labor economists have been tracking other data to complement BLS surveys signaling a cooling labor market, particularly unemployment insurance claims and JOLTS. However, claims have shown no substantial increases in the following weeks since July, and neither have separations.

| year | Period Name | value | Lagged Year Value | Over Year Change | Lagged Month Value | Over Month Change | Over Year Change |

| 2024 | July | 5,420 | 5,646 | -4.2 | 5,084 | 6.2 | 226 |

| 2023 | July | 5,646 | 5,852 | -3.6 | 5,639 | 0.1 | 206 |

| 2022 | July | 5,852 | 5,826 | 0.4 | 5,980 | -2.2 | -26 |

| 2019 | July | 5,839 | 5,577 | 4.5 | 5,574 | 4.5 | -262 |

| 2018 | July | 5,577 | 5,338 | 4.3 | 5,566 | 0.2 | -239 |

| 2017 | July | 5,338 | 5,065 | 5.1 | 5,463 | -2.3 | -273 |

| 2016 | July | 5,065 | 4,848 | 4.3 | 5,118 | -1.0 | -217 |

| 2015 | July | 4,848 | 4,748 | 2.1 | 4,978 | -2.7 | -100 |

| 2014 | July | 4,748 | 4,421 | 6.9 | 4,612 | 2.9 | -327 |

| 2013 | July | 4,421 | 4,151 | 6.1 | 4,307 | 2.6 | -270 |

| 2012 | July | 4,151 | 4,153 | 0.0 | 4,382 | -5.6 | 2 |

| 2011 | July | 4,153 | 4,269 | -2.8 | 4,173 | -0.5 | 116 |

| 2010 | July | 4,269 | NA | NA | 4,311 | -1.0 | 226 |

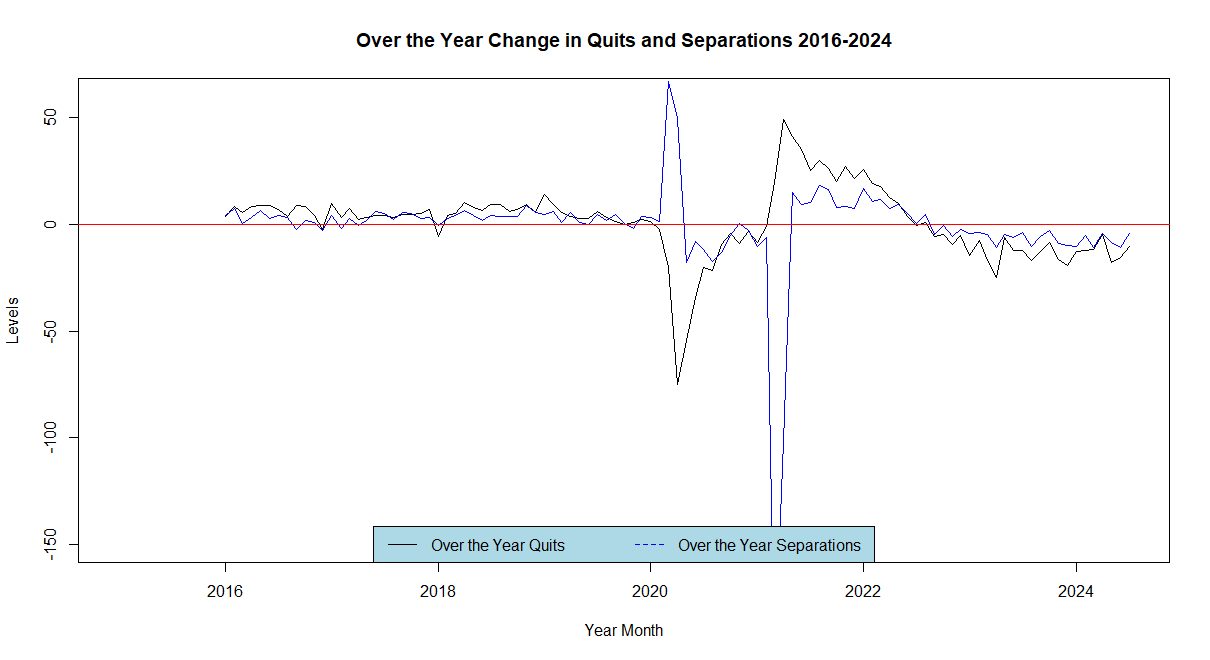

Quits and Separations came strong to the current narrative because the economic concern after the Pandemic has been an overheated Labor Market where Quits were extremely high while Separations were low. Labor Economist have been tracking Quits and Separations for two reasons, first to assess the tightness of the Labor Market, and second to evaluate the effect of restrictive monetary policy. The evidence is clear as everybody seems to agree that the market has softened. However, Separations do not deliver insights on the link that worries the Federal Reserve, wage inflation as a driver of Shelter inflation. In fact, data show that the economy is exactly in the same state as it has been since the beginning of the year. These data still leave the balance of risk on the inflation side.

Make an Appointment Now

Categories: Macroeconomics

1 reply »